What is driving inflation in Malaysia? For the last four months of 2021, the CPI jumped a full two points, or 1.6%, which is equivalent to an annualised increase of 5%. That would mark the strongest annual inflation reading since 2008, when the lifting of price controls on RON95 petrol saw it hitting RM2.70.

If you read yesterday's post, you'll suspect its food and petrol, and you would be mostly right. There is however some nuance here. To satisfy my curiosity, I cut the data based on different time periods, looking at the contribution of each COICOP category to total inflation:

For the full 2010-2021 period, 49.6% of inflation came from just food alone. Looking at the subgroups, its also clearly mostly fish & seafood and vegetables, and food away from home. The other big contributors are transport (ie mostly petrol) and housing & utilities. The three main groups of food, housing, and transport combine for 67.5% of average household expenditure, but contributed 79.8% of the increase in prices since 2010.

For the other two periods, I took the latest 4 month time frame (basically from when inflation started to pick up), and the rather curious spurt of inflation at the end of 2020. There's some differences here, as the 2020 jump in prices - which incidentally was even stronger than the current one at 7.4% annualised - was mainly due to the increase in RON95 prices. Contrast that with the latest inflation episode, which more closely conforms to more "normal" inflation dynamics.

In all cases however, roughly 80% of inflation comes from just these three sources, none of which can truly be said to be domestic demand driven, with the exception of housing. So there's some evidence of demand led inflation which would necessitate a monetary policy response, at least domestically. I'd still consider it pretty weak however, given the weakness in the other groups, especially recreation, education, and restaurants & hotels, where prices are more directly driven by the cost of labour.

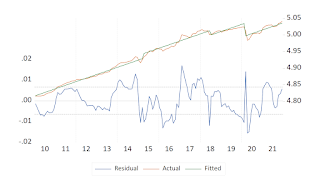

Part of the problem of interpreting the CPI is of course the role of price controls, particularly on specific food items and petrol. But that's neither here nor there, given that core inflation is right on the long term average, and the price level is rising roughly around its long term trend line (taking the drop due to Covid into consideration):

The bigger question of course is whether fiscal and monetary stimulus should start to be withdrawn. I'll leave that for a future blog post.

No comments:

Post a Comment